When a health emergency strikes, the financial fallout can feel like an unexpected storm—unpredictable and potentially overwhelming. In 2026, patients seeking to cover elective procedures, fertility treatments, or unforeseen hospital bills have more options than ever, but each comes with its own set of terms, rates, and eligibility criteria. By understanding how medical loans differ from traditional personal loans and knowing where to look for the best offers, borrowers can make informed decisions that keep their health—and wallet—intact.

Loan Now: Loan Now

The Rise of Medical‑Specific Lending

Medical loans have carved out a niche within the broader personal lending market. Unlike conventional personal loans, which are typically unsecured and aimed at general debt consolidation or home improvement, medical loans focus exclusively on health-related expenses. This specialization allows lenders to tailor interest rates, repayment terms, and eligibility requirements based on the unique risk profile of healthcare costs.

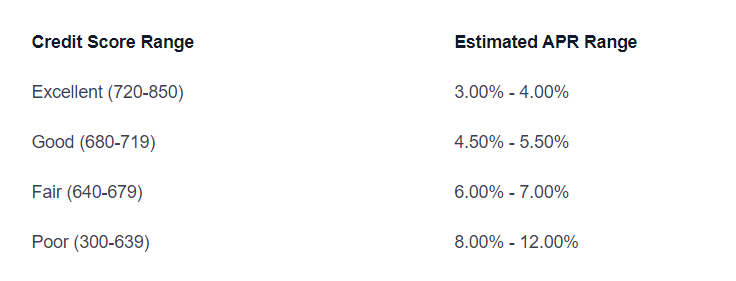

In 2026, the average APR for a medical loan can range from as low as 7.74% to over 35%, depending largely on credit score and lender policy. For borrowers with excellent credit (720–850), rates near the lower end are attainable, while those with fair or poor credit may face steeper costs. This spectrum mirrors trends seen in broader personal lending markets, where higher risk translates into higher interest.

The market has also expanded beyond banks to include credit unions, online lenders, and even specialized health‑care financing companies such as CareCredit. Each player brings distinct advantages: credit unions often offer lower fees; online platforms provide instant approval; while health‑specific issuers may grant promotional no‑interest periods for certain procedures.

How Medical Loans Compare to Other Financing Options

- No-Interest Promotions: Many medical lenders, like CareCredit, offer six-, twelve-, eighteen-, or twenty-four-month promotional periods with zero interest. If you pay off the balance within that window, you avoid any additional cost.

- Collateral Flexibility: While most medical loans are unsecured, some institutions allow secured variants backed by assets such as a vehicle or savings account, potentially lowering APRs for those who qualify.

- Loan Amount Limits: Medical loan providers typically offer amounts ranging from $1,000 to $50,000. This range is comparable to personal loans but can be more generous for elective procedures that require larger upfront payments.

- Application Speed: Online lenders often fund within one business day, whereas traditional banks may take several days or weeks—an important factor when medical bills pile up rapidly.

Key Metrics to Watch When Shopping for a Medical Loan

Borrowers should scrutinize three core elements: APR, origination fees, and repayment flexibility. A seemingly attractive low rate may be offset by high upfront charges or rigid repayment schedules that strain monthly budgets.

| Metric | Description |

|---|---|

| A.P.R. | Annual percentage rate, inclusive of interest and fees. |

| Origination Fee | One‑time charge, often expressed as a % of the loan amount. |

| Repayment Terms | Duration (2–7 years) and flexibility to adjust payment dates. |

Sources such as NerdWallet’s aggregated data confirm that for borrowers with a credit score above 600, the average APR sits around 14.48% across all personal loan types—including medical loans—highlighting the importance of credit health in securing favorable terms. NerdWallet Average Rates

Eligibility: Credit Scores and Beyond

Credit score remains the primary gatekeeper for medical loan approval. Lenders typically require a minimum of 600, but many prefer scores above 650 to lock in lower rates. Those with no credit history can still find options; certain lenders accept applicants without prior credit records or even allow co‑signers with stronger credit.

Beyond score, income verification and employment stability are standard prerequisites. Lenders will often request recent pay stubs, tax returns, or bank statements to confirm the borrower’s capacity to repay. In cases where debt consolidation is the goal, lenders may also evaluate existing balances on credit cards or other loans.

A practical tip: before applying, run a soft credit check through an online pre‑qualification portal—many lenders offer this without impacting your score. This gives you a realistic estimate of the rate range you might receive and helps avoid surprise rejections. Credit Karma Medical Loan Pre‑Qual

Special Considerations for Health‑Care Providers

Some health‑care facilities partner directly with financing companies, offering integrated payment plans that align with insurance coverage. These arrangements can reduce out‑of‑pocket costs by aligning the loan balance with any remaining deductible or co‑payment amounts.

For elective procedures such as cosmetic surgery or fertility treatments, providers may also offer “no‑interest until a certain date” plans, effectively functioning as in‑house credit cards. While convenient, these often come with higher overall interest if balances are not paid off promptly.

Choosing the Right Lender: A Comparative Snapshot

Below is a concise comparison of three prominent medical loan options available in 2026, highlighting key differentiators for borrowers seeking the best fit.

| Lender | APR Range | Loan Amount | Origination Fee | Repayment Terms |

|---|---|---|---|---|

| Upgrade | 7.74% – 35.99% | $1,000–$50,000 | Up to 5% | 2–7 years |

| LendingClub | 5.96% – 35.99% | $1,000–$60,000 | None (soft credit check) | 2–7 years |

| CareCredit | No interest promotional periods; then variable APRs | $1,000–$50,000 | None (card‑style fee) | Fixed 24‑month plans |

While Upgrade offers robust rate discounts and a quick funding window of one day, LendingClub’s absence of an origination fee can be appealing for borrowers wary of hidden costs. CareCredit remains the go‑to choice for those who prefer a credit‑card–like experience with promotional no‑interest periods.

Impact of Credit Score on APR and Approval Odds

Data from CNBC Select’s 2026 roundup shows that applicants scoring below 670 are still eligible for certain lenders, but the APRs climb as risk perception increases. For instance, a borrower with a score of 640 may face an average rate around 25%, while one with 700 might secure rates near 12–14%.

Moreover, co‑signers can dramatically shift the approval odds. A strong co‑signer’s credit profile effectively mitigates lender risk, often unlocking lower APRs and higher loan limits. This strategy is especially useful for younger borrowers or those rebuilding credit. CNBC Select Loan Lenders

Strategies to Improve Your Credit Standing Before Applying

- On-Time Payments: Consistently paying bills in full and on time boosts payment history, the largest factor in credit scoring.

- Reduce Debt-to-Income Ratio: Lowering existing balances relative to income signals financial responsibility.

- Avoid New Credit Lines: Opening multiple new accounts in a short span can lower scores; focus on maintaining stable credit history.

If you’re planning ahead, consider setting up automatic payments. Many lenders offer slight APR reductions for autopay, and it also guards against missed due dates that could trigger late fees.

Conclusion: Making the Right Choice in a Complex Market

In 2026, medical loans have matured into a sophisticated segment of personal finance, offering tailored solutions for health‑care expenses. By evaluating APRs, origination fees, repayment flexibility, and eligibility criteria—and by leveraging pre‑qualification tools—borrowers can navigate this landscape with confidence. Whether you’re financing an emergency procedure or planning elective surgery, the right loan can help keep your medical bills manageable while preserving financial stability.